Should WeWork really be worth $20 billion?

On January 1st, 2018, not only will it be a new year, IE will have a new neighbor a few blocks down the Paseo de la Castellana from María de Molina: WeWork. As they were putting the floors in the new Madrid space, WeWork was about to make a significant splash. Back on the homefront in New York City, HBC announced last week that WeWork will purchase the iconic Lord & Taylor flagship store building in Midtown Manhattan right on Fifth Avenue for $850 million. HBC is the Hudson’s Bay Corporation, the owner of department stores such as Saks Fifth Avenue and Lord & Taylor in the United States, Galeria Kaufhof in Germany, and Hudson’s Bay in Canada. After the holiday season in 2018 and WeWork moves in, the retail space in the building will go down to 150,000 square feet from the total 675,000 square feet Lord & Taylor occupied a century ago. While the deal highlights the retail industry’s challenges in making use of excess brick and mortar space, the real question is this: how did WeWork get here?

So, what’s WeWork and why do we care?

If Silicon Valley is the home for startups in the United States, WeWork is the top dog on the New York City startup scene, not to mention that it’s the third most highly-valued startup in the United States (after two players named Uber and Airbnb). So, what’s WeWork anyway? WeWork “…leases trendy, millennial-friendly office space to startups and Fortune 500 companies.” Not only is it one of the top-valued startups in the United States, but it’s also rightly taken its place among the world’s best: it recently became the 6th most valuable startup worldwide.

In 2001, WeWork’s founders, Israeli entrepreneur Adam Neumann and American architect Miguel McKelvey, met in the office building where they were both mutually working. In 2008, the two created GreenDesk in a building on Water Street in Brooklyn’s Dumbo neighborhood, an early incarnation of the WeWork concept. As the financial crisis worsened, laid-off professionals rented space at GreenDesk to start new businesses. GreenDesk offered everything someone would need for an office space and users paid monthly to use it at prices that were more expensive than what Neumann and McKelvey were paying in rent. The two posited that the most valuable part of GreenDesk was the community, and after selling GreenDesk, they rented a floor in a Soho building in 2010 to become the first WeWork.

What was the rationale behind WeWork? Here it is: “[e]arly on, Neumann and McKelvey imagined office rentals as part of an ecosystem, complete with apartments, gyms, and even barber shops, that served the concept of a communal life.” A month into the lease, the first WeWork turned a profit, and it became a gathering spot for investors, developers, and the nexus for growing the WeWork brand. Across 18 countries, WeWork today has 165 offices (with Madrid and Barcelona next year) and more than 150,000 members. Every WeWork space has a different look but with a similar layout, with community perks no matter the type of office space you choose to rent as a WeWork member.

So, just how much funding has it raised? According to a Business Insider article from September 2017, WeWork had raised over $8 billion, with $4.4 billion coming in since July 2017, at that $20 billion valuation.

Why people believe WeWork’s worthy of the $20 billion valuation

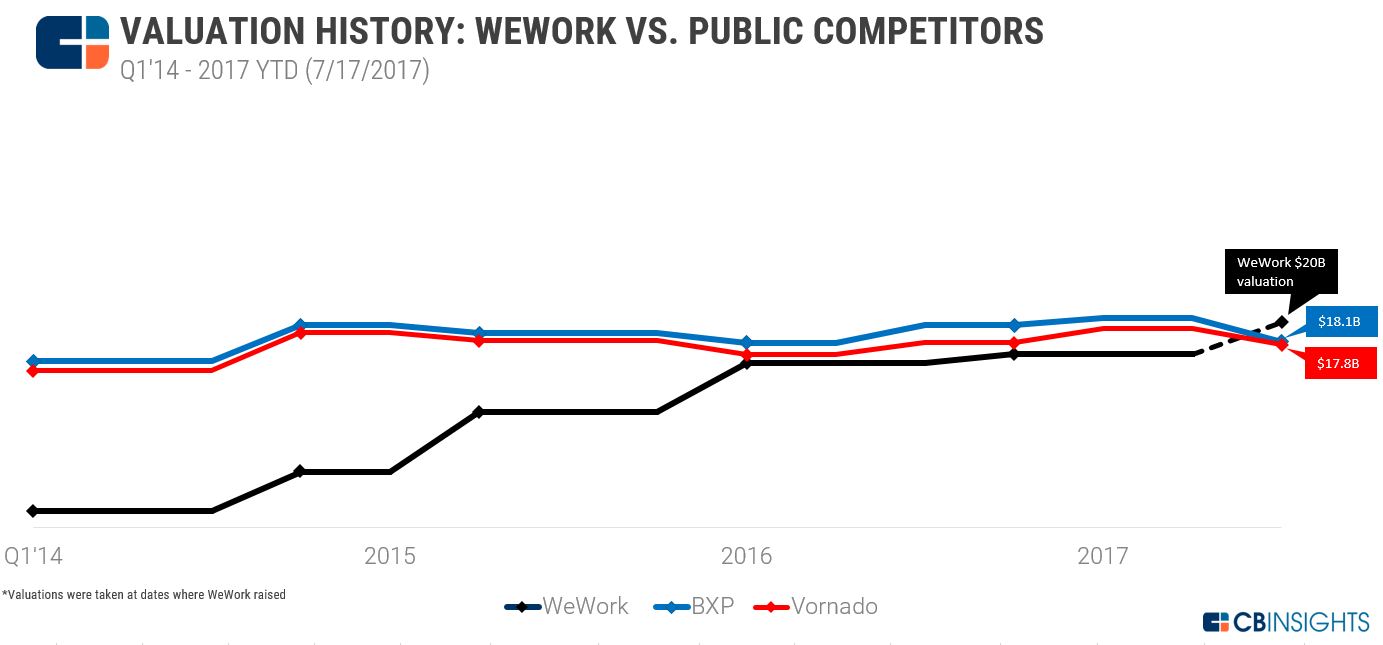

To get the scoop and relate it to the hardcore numbers behind a valuation, we turned to a report from CB Insights. First things first, WeWork, like other well-known startups such as Dropbox and Blue Apron, is one of those elusive unicorns in startup terminology. In the fourth quarter of 2014, WeWork became a unicorn after successfully raising $175 million in a Series C round from investors that included JP Morgan Chase and Benchmark Capital with a valuation of $1.59 billion. To get at the heart of WeWork’s valuation, CB Insights compared the startup to real estate mainstays that include Boston Properties, Regus, and Vornado.

Today, with the estimated $20 billion valuation, WeWork is now more valuable than both Boston Properties ($18.18 billion) and Vornado ($17.88 billion):

Source: CBInsights

How did they get there?

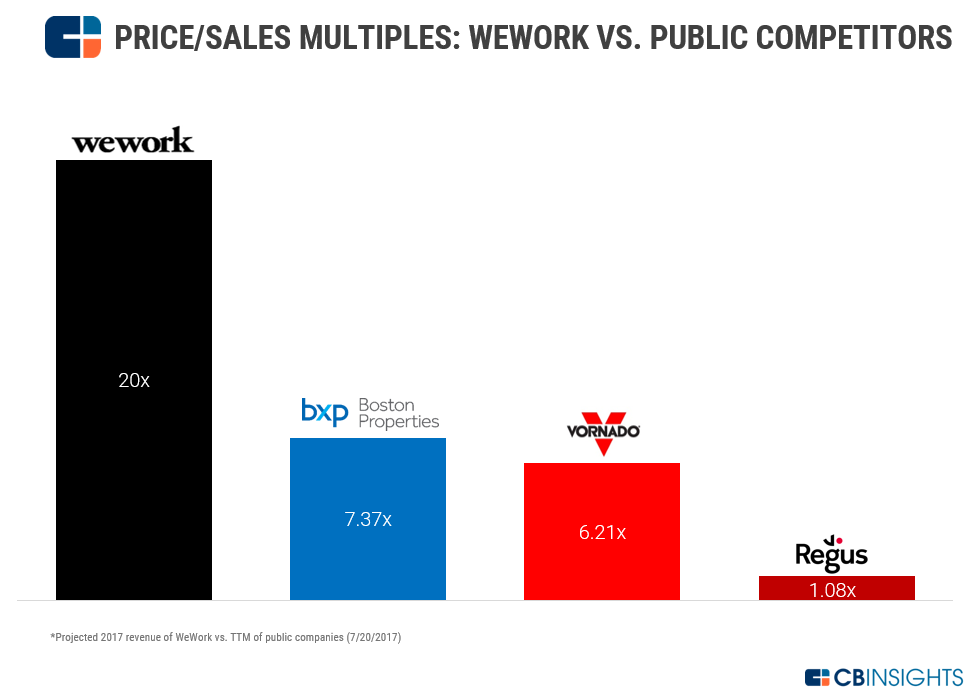

First, CB Insights calculated the price-to-sales (P/S ratio) to get the multiples between WeWork, Boston Properties, Regus, and Vornado. Why look at this rate? The P/S ratio offers a simple way for an investor to compare stock prices: you “…take the company’s market capitalization (the number of shares multiplied by the share price) and divide it by the company’s total sales over the past 12 months. The lower the ratio, the more attractive the investment.” When looking at the multiple in the chart below, you can see that for data on July 20th, 2017, WeWork’s price/sales multiples was 20x, nearly 18x that of its closest market competitor, Regus:

Source: CBInsights

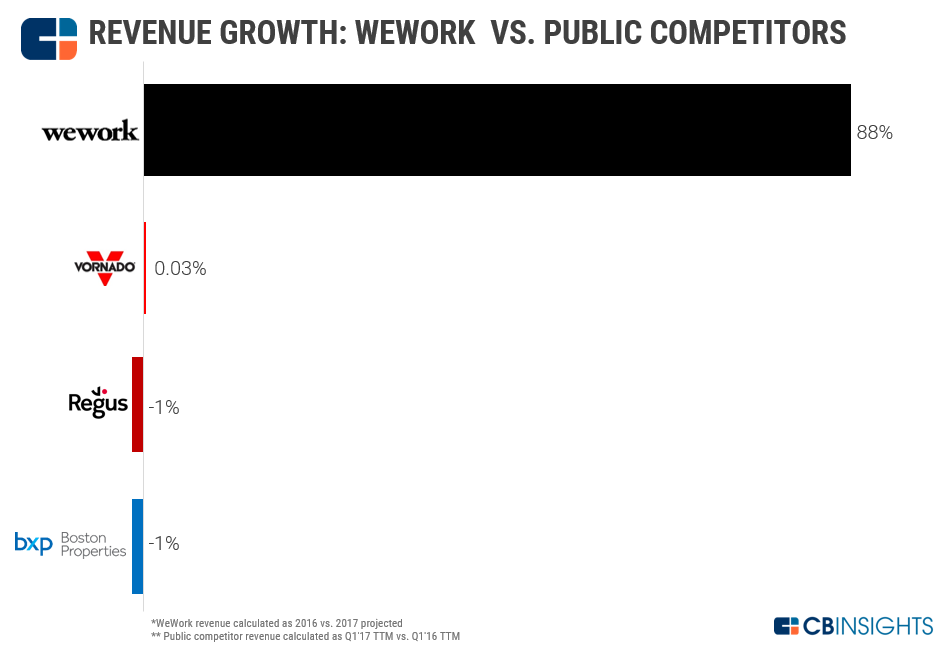

Next, compared to public competitors (Boston Properties, Vornado, and Regus), WeWork’s revenue growth is outpacing the rest, by a dramatic amount

Source: CBInsights

Despite the fact WeWork is only raking in a fraction of the revenue that public competitors are getting and the numbers are contingent on them reaching $1 billion in revenue in 2017, they’re experiencing significant growth. In contrast, all public competitors are seeing their revenue growth rates decrease by 1%, or just about flat in the case of Vornado, while WeWork’s revenue is growing at 88%. Remember, the stock price looks at the expected future value of the current business!

Other points of argument are the following: “Defenders of WeWork’s rich valuation note that the company is bringing in revenue by providing core services and community benefits, growing their enterprise sales (which account for “30% of new business), expanding globally, and diversifying their revenue streams as previously mentioned.”

Why others believe WeWork is the most overrated startup

Many investors and real estate industry insiders are quick to note that while WeWork is a real estate company, they fund themselves as if they’re a tech company. From their perspective, they’re“…simply occupying a niche within the real estate market of ‘space-as-a-service.’” While CEO Adam Neumann has refused to label WeWork as a real estate of a tech company and instead give it the moniker of a community company, there are reports that they’re reconsidering the company’s classification.

The next reason why people are quick to think of WeWork as overrated is the fact that the success of their business model is heavily dependent on not only the real estate industry but also tech. The flexible leasing agreements are ideal for smaller companies, but if another economic downturn similar in scope to the 2008 financial crisis were to come about, it could spell trouble.

When it comes to tangible assets, WeWork doesn’t have any. That’s because“WeWork does not currently own any property; the company takes long-term leases and rents those properties out at a higher value than their lease payments by adding rental and office management fees (cleaning, internet, events, etc.) begging the question how a company with such a high valuation doesn’t own any tangible assets.”

And many naysayers don’t think that the business model is disruptive enough. That’s because of Regus, the closest public competitor to WeWork, that has a similar business model based on renting out co-working spaces, and not only that, it may just follow the natural growth and recession patterns in the rest of the economy.

If you want a view from a naysayer institutional investor, NYU Stern School of Business Marketing Professor Scott Galloway (who’s also the founder of business intelligence firm L2) talked about why he thinks WeWork is overrated in a recent video interview with Business Insider:

How WeWork’s working to prove the naysayers wrong

Along with reconsidering their categorization, WeWork’s transition from relying on startups “…to large corporates like IBM, thus mitigating potential risks of being unable to sustain rental agreements.” When it comes to the lack of owning property, they recently helped a real estate investment fundraise hundreds of millions of dollars, and they’ve also announced their plans for acquiring buildings where they are currently leasing space.

The most significant point where they’re looking to prove naysayers wrong is their expansion of their business model into new concepts. One is WeLive, which offers apartments and a plethora of communal amenities with one building in New York’s Financial District and Crystal City in Arlington, Virginia in the Washington, DC Metro Area. The next prong is fitness, with the Rise by We fitness facility opening in WeWork’s Financial District location in New York City. You don’t have to be a WeWork member to join. If you join Rise by We and not WeWork, you’ll get “…access to WeWork’s digital member network, plus two credits per month to book conference rooms or workspace in select WeWork locations.” They’ve also made moves into the facilities management areain the real estate sector. These new services, therefore, would prove that they are in fact disrupting the traditional co-working space model.

What’s the verdict?

Well, that’s for you to decide, but to give you some food for thought, we’ll leave you with conclusions from the experts. Here’s what CB Insights had to say: “If WeWork can manage to hit its $1B projected revenue target for 2017, continue increasing enterprise sales, and successfully diversify its revenue streams locally and abroad, the company definitely has a shot to justify its $20B valuation.”

Ready to get the tools to see if you agree with WeWork’s $20 billion valuation?

If you’re eager for facts about corporate valuation in the Embedding Finance in Everyday Decision Making HiOP, download your informational brochure. If you’re already set on joining us, get started on your application right now.